Let’s be honest: thinking about retirement can feel like staring into a crystal ball filled with financial jargon. You hear about 401(k)s , IRAs, and Social Security , and it all starts to blur together. But here’s the thing: your 401(k) isn’t just some abstract retirement fund. It’s a powerful tool that can shape your financial future. And understanding it – really understanding it – is the first step to taking control.

This isn’t just another article regurgitating the basics. We’re diving deep. We are going to explore why your 401(k) matters, how to make the most of it, and tackle some common misconceptions along the way. Think of this as your friendly, no-nonsense guide to mastering your retirement savings .

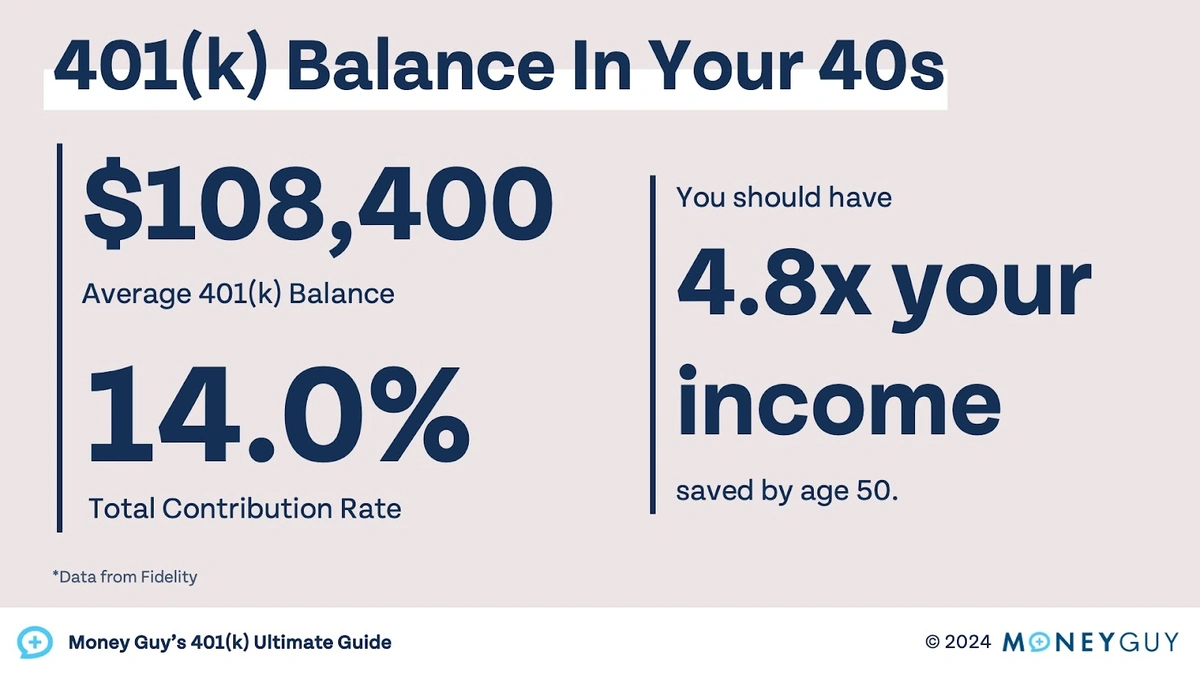

The “Why” Behind Your 401(k) | More Than Just Matching Contributions

So, what is a 401(k) anyway? In a nutshell, it’s a retirement savings plan sponsored by your employer. You contribute a portion of your paycheck, and often your employer will match a percentage of your contribution. But here’s where the “why” gets interesting. It’s not just about the matching funds (although, free money is always a good thing!). Your 401(k) offers significant tax advantages.

Contributions are typically made on a pre-tax basis, meaning you don’t pay income tax on the money until you withdraw it in retirement. This can lower your taxable income now . Plus, your investments grow tax-deferred, which allows your money to compound faster. Imagine the possibilities. The beauty of compound interest, like a snowball rolling downhill, gathers momentum and size.

And, it’s not just for the traditional employer-sponsored type. There’s also something called the self-employed 401k, which is also known as a solo 401k. If you’re a freelancer or small business owner, this is an option for you.

Maximizing Your 401(k) | Beyond the Basics

Okay, you know why a 401(k) is important. Now, how do you make the most of it? A common mistake I see people make is simply enrolling and then forgetting about it. Let’s be honest, most of us don’t know much about investment options , and how to determine which funds best suit our goals and risk tolerance.

First, aim to contribute enough to get the full employer match. This is essentially free money, and leaving it on the table is like turning down a raise. Then, consider increasing your contribution percentage gradually over time. Even a small increase can make a big difference in the long run.

Next, pay attention to your asset allocation . This refers to how your investments are spread across different asset classes, such as stocks, bonds, and real estate. Diversification is key to managing risk. Don’t put all your eggs in one basket. If you’re unsure where to start, consider using a target-date fund, which automatically adjusts your asset allocation as you get closer to retirement.

It’s also important to rebalance your portfolio periodically. As your investments grow, your asset allocation may drift away from your target. Rebalancing involves selling some assets and buying others to bring your portfolio back into alignment. Finally, don’t forget to periodically review your account statements and monitor your investment performance. Stay informed and make adjustments as needed. Planning for retirement may sound daunting, but with careful planning and a long-term perspective, you can build a secure and comfortable future.

Common 401(k) Myths Debunked

There are plenty of myths surrounding 401(k)s that can prevent people from taking full advantage of their retirement savings. Let’s bust a few of the most common ones.

Myth #1: “I’m too young to worry about a 401(k).” Wrong! The earlier you start saving, the more time your money has to grow. Time is your greatest asset when it comes to investing. According to the Securities and Exchange Commission , investing even small amounts early can make a big difference.

Myth #2: “I can’t afford to contribute to a 401(k).” I understand that saving money can be tough, especially when you’re just starting out. However, even contributing a small percentage of your paycheck can make a difference. Plus, many employers offer matching contributions, which essentially doubles your savings. If you can’t afford much, start small and gradually increase your contributions as your income grows.

Myth #3: “My 401(k) is all I need for retirement.” While a 401(k) is an important part of your retirement plan, it shouldn’t be your only source of income. Consider supplementing your 401(k) with other savings and investments, such as an IRA or taxable brokerage account. And don’t forget about Social Security. Understanding your estimated Social Security benefits is crucial for planning your retirement income.

401k Withdrawal Strategies | Planning for the Future

Thinking about drawing from your 401k funds ? Here’s where things get interesting. Generally, you want to wait until retirement age to avoid penalties, but life happens. Knowing the rules before you need them is crucial.

First off, early withdrawals (before age 59 1/2) usually come with a 10% penalty, plus you’ll owe income tax on the amount you withdraw. Ouch! There are exceptions, though. Some situations, like certain medical expenses or financial hardships, might allow you to avoid the penalty. It’s best to consult with a financial advisor or tax professional to understand your options and the potential consequences. Additionally, be aware of the required minimum distributions (RMDs) that begin at age 73. Not taking these distributions can result in penalties, so it’s essential to plan ahead and understand the rules.

Navigating 401(k) Rollovers | Keeping Your Savings on Track

Changing jobs? One of the first things you should consider is what to do with your 401(k) from your previous employer. You have a few options. You can leave the money in your old employer’s plan (if allowed), roll it over into a new employer’s plan, roll it over into an IRA, or cash it out (not recommended due to taxes and penalties).

Rolling over your 401(k) into an IRA can offer more investment flexibility, but it’s essential to compare fees and expenses. Before making any decisions, assess your financial goals, risk tolerance, and investment options. A well-executed rollover can help you maintain control over your savings and continue building toward a secure retirement. The overall investment strategy and plan will contribute to your success.

FAQ | Your Burning 401(k) Questions Answered

Frequently Asked Questions

What if I change jobs?

You can roll over your 401(k) to your new employer’s plan, an IRA, or leave it with your previous employer (if the plan allows).

Can I borrow from my 401(k)?

Yes, but it’s generally not recommended. You’ll have to pay the loan back with interest, and if you leave your job, the outstanding balance may be treated as a distribution, subject to taxes and penalties.

What happens to my 401(k) if I die?

Your 401(k) will pass to your designated beneficiaries. The tax implications will depend on the beneficiary’s relationship to you and the type of account.

How often should I review my 401(k) investments?

At least once a year, or more frequently if your circumstances change or the market is volatile.

Your 401(k) is more than just a retirement account. It’s a tool for building a secure financial future. By understanding the “why” behind it, maximizing your contributions, and avoiding common pitfalls, you can take control of your retirement savings and create the future you deserve. Start today – your future self will thank you. Building long-term financial security is possible!

{kind=link}